Mar 16, 2026

Why member behavior just became a P&L item

8 min read

The operating environment has fundamentally changed

Health plan margins are at their lowest in two decades.1 Medical cost trend is projected at 8.5% for 2026.2 MA plan terminations affected 13% of MA-PD enrollees in 2025 — the highest rate on record.3 And H.R. 1 has tightened Medicaid eligibility and redetermination timelines.4

I’ve spent over a decade building League, and in that time I’ve watched health plans build portals and buy point solutions that were designed to record transactions, not move member behavior at scale. But there’s more urgency than ever to deploy solutions that drive action. What’s changed is that policy has put a price tag on that failure and the timelines are fixed.

Stars methodology is shifting. The CY2027 final rule reduces administrative process measures and increases the weight of member experience and clinical outcomes, the two domains most directly driven by engagement.10 With $12.7B in MA bonus payments at stake, falling below 4 stars eliminates quality bonus revenue entirely and drops rebate retention from 65% to 50%.9 For large plans, that’s a potential revenue swing of hundreds of millions in a single ratings cycle.

H.R. 1 doubles redetermination frequency for Medicaid expansion populations to every six months, effective December 2026. The Congressional Budget Office estimates 700,000 people will lose coverage by 2034 — 70% for procedural reasons (i.e. missed paperwork, communication barriers, poor navigation), not ineligibility.13 Every missed form, unreturned call, or language barrier is lost capitation on a member who was still eligible.

State requirements are fragmenting the compliance landscape. In 2025, 37 states introduced new health equity legislation.11 California’s CalAIM, which mandates Health Equity Accreditation, whole-person care management, and multilingual engagement, is the most advanced expression of a trend that is spreading across multi-state operators.

These aren’t separate headwinds. They’re the same storm. These three policy shifts are signals that the way plans need to manage member action is fundamentally changing. What members actually do – or don’t do – will show up directly in P&L statements. Member behavior is the next cost lever, and it is also the one lever traditional approaches have not been able to move at scale.

The cost of inaction is measurable

There’s a lot on the line if plans don’t take action now. Avoidable medical costs total roughly $79 billion annually, driven largely by members who don’t understand their benefits, don’t see their PCP, and don’t manage chronic conditions. 40% of Medicare beneficiaries remain chronically disengaged from basic preventive care.6

And traditional approaches trying to solve these problems are falling short. Legacy portals deliver information but not guidance because they don’t know what a specific member needs to do next, and they can’t reach them in the language or channel that will actually drive action. Paper outreach misses the populations these plans serve most: multilingual, mobile-first, time-constrained members for whom a form in the mail is not a pathway to action. Call centers can’t scale to the volume and complexity these populations require.

These operational costs compound into a clinical one. When no single system owns what should happen next, plans pay to do the same work multiple times: redundant outreach across channels and repeat call volume from members who couldn’t find an answer the first time. In the end, outcomes suffer.

Traditional levers can’t close the gap either. Utilization management, network steerage, and care management programs have stabilized trend lines but can no longer deliver the step-function change required to protect margins.7

Member experience is operational infrastructure

Every one of the policy shifts above comes down to the same problem: getting the right member to take the right action at the right time. Stars move when a member completes a preventive visit or closes a care gap. Medicaid revenue holds when an eligible member renews before the deadline. And no portal, call center, or point solution was built to solve it at scale.

What’s missing is an AI-native platform built with intelligent orchestration that owns what should happen next and connects a member’s unique circumstances to the specific action that reduces costs, extends their coverage, and improves their health outcome. It unifies what the plan knows about each member across eligibility, claims, clinical contexts and social determinants data into a single picture of that person and uses that to anticipate, personalize, and act at population scale, across every member, every single day.

Over time, members who are consistently met with guidance that’s actually relevant to them complete more of the actions that protect quality scores, capitation revenue, and renewal, and stay connected to their plan when it matters most.

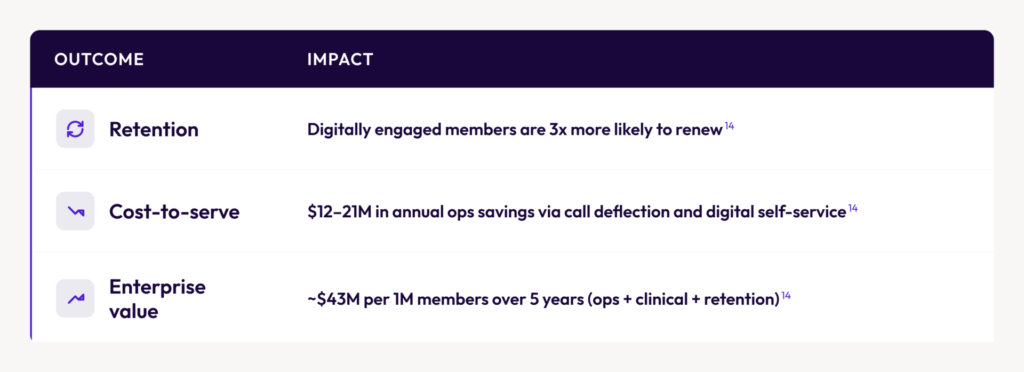

The financial impact of this new model is direct and measurable:

Plans already deploying this type of platform are seeing the impact. A blinded regional Medicaid plan deployed at 1/6 the cost and 1/3 the time versus their internal build estimate.15 SCAN Health Plan achieved 37% monthly active users, 54% MAU growth in two quarters, and 82% of members rating their experience 7/10 or higher.15 Santa Clara Family Health Plan achieved 3x digital activation, 68% member satisfaction, and 7 languages supported natively.15

Why now

Plans are entering the execution window now. The Stars methodology shift is locked into the CY2027 final rule. H.R. 1 redetermination requirements are effective December 2026. State-level equity and engagement requirements are already in-market.

The plans that will differentiate on member satisfaction, retention, and operating efficiency are the ones building infrastructure that actually gets members to act, reaching them in their language, guiding them through the specific actions that carry financial and quality weight, at a scale call centers and legacy technology never could. The plans that do not make the shift will face a compounding disadvantage, year over year, as the financial weight of member action increases.

More importantly, the members these plans serve — elderly, low-income, multilingual, often navigating the hardest moments of their lives — will finally have a health experience built around their needs.

See how League is purpose-built for this moment

Plans that build this infrastructure now will be a full performance cycle ahead. The ones that wait face a compounding disadvantage that gets harder to close every year.

Sources

1. PwC, Future of Payers: Half the Cost, Twice the Service, 2025.

2. PwC, Behind the Numbers 2026: No Let Up in Sight, July 2025.

3. KFF, Most Medicare Beneficiaries Affected by Plan Terminations in 2025 Have Robust Medicare Advantage Options in 2026, March 2026.

4. KFF, Medicaid: What to Watch in 2026, January 2026.

5. Engagys, How Payers Can Reduce Medical Costs Through Member Engagement, December 2025.

6. Pareto Intelligence, Improving Member Engagement in Medicare Advantage Rewards, December 2025.

7. Engagys, Engagement is the New Cost Lever, September 2025.

8. HealthEdge, AI in 2026: Are Health Plans and Members Aligned on the Future?, February 2026.

9. KFF, Medicare Advantage Quality Bonus Payments Will Total at Least $12.7 Billion in 2025, June 2025.

10. CMS, Contract Year 2027 Medicare Advantage and Part D Final Rule, April 2026.

11. HealthScape Advisors, States Are Staying the Course on Health Equity Policy, February 2026.

12. Atlas Systems, Network Adequacy 2026: Medicare & Medicaid Requirements, 2026.

13. Georgetown University, New CBO Health Coverage Estimates of Budget Reconciliation Law, February 2025.

14. League Value Repository; financial claims modeled off customer results.

15. League customer data — SCAN Health Plan; Santa Clara Family Health Plan; regional Medicaid plan (blinded). Approved for external use.